Executive Summary: The US–Mexico–Canada Agreement (USMCA) enters a mandatory review by July 1, 2026, triggering negotiations that could reshape North American autos. U.S. Trade Representative Jamieson Greer opened talks with Mexico (March 2026) and will meet Canada (May 2026)[1][2]. President Trump’s 2025 imposition of 25% tariffs on all autos (with partial carve-outs for USMCA-originating content) and 50% steel/aluminum tariffs has already added ~$30 billion to U.S. auto costs[3][4] and spurred significant shifts in production. Key negotiation issues include raising content rules (Regional Value Content and Labor Value Content), tightening steel/aluminum sourcing (now 70% NA origin[5]), adjusting the 10% de minimis allowance[6], and clarifying parts classification (especially EV components)[7]. Automakers and suppliers warn that uncertainty and tariffs are driving up costs and destabilizing investment plans[8][9]. Trade flows are deeply integrated: Canada and Mexico supply ~45% of U.S. auto imports and take ~75% of U.S. auto exports[10] (see Figure below)[10]. Any tightening of origin rules would expose more vehicles/parts to high (25%) tariffs. For example, studies show raising RVC beyond 75% modestly reduces U.S. vehicle output (~15,000 units) while boosting parts output and investment[11]. Unions (e.g. USW, UAW) and manufacturing groups (AAM, Alliance) demand stricter rules to curb “backdoor” Chinese auto content via Mexico and raise wages[12][13]. Short-term impacts include higher vehicle prices and disrupted sourcing; medium-term could see some production shift toward the U.S. and factory investments in flux. Long-term outcomes hinge on scenario: a “renewed” USMCA (best case) preserves supply chains; a “painful extension” (likely) forces higher content and inflationary costs; withdrawal (worst) invites trade wars and fragmentation. Quantitatively, U.S. auto imports from Canada/Mexico (~$189B in 2024[10]) would face tariffs on any non-originating share, raising prices by thousands per vehicle[3]. We summarize impacts on jobs (U.S. auto supports ~11M jobs[14]), wages (Mexico’s auto wages remain far below U.S. levels[12]), and investment (major planned U.S. auto plants conditional on stable rules[8]). Key industry and labor statements are detailed below. Policymakers and firms should plan for all scenarios: strengthen domestic content and worker training, maintain cross-border supply integration, and push for predictable rules.

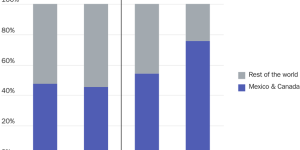

Figure: North American integration in automotive trade. The U.S., Canada and Mexico form a highly integrated supply chain: together they supplied nearly half of U.S. vehicle and parts imports (left chart) and received roughly three-quarters of U.S. auto exports (right chart) in 2024[10]. Disruptions in USMCA rules would thus affect a vast $270B auto trade corridor.

Figure: North American integration in automotive trade. The U.S., Canada and Mexico form a highly integrated supply chain: together they supplied nearly half of U.S. vehicle and parts imports (left chart) and received roughly three-quarters of U.S. auto exports (right chart) in 2024[10]. Disruptions in USMCA rules would thus affect a vast $270B auto trade corridor.

Timeline of Negotiations (July 2025–July 2026)

- March–May 2026: Bilateral talks began: U.S.–Mexico meetings started in mid-March[15]; U.S.–Canada talks began in early May[2]. Canada’s Trade Minister LeBlanc reported “constructive” discussions with U.S. Trade Rep. Greer[1]. USTR Greer signaled that Washington aims to “resolve as many problems…before July 1,” but expects talks to extend beyond that date[2][16].

- June 1, 2026: By law, the U.S. must notify Congress of its intention to extend or withdraw from USMCA[16].

- July 1, 2026 (Deadline): The formal joint review target. All three parties must either agree to extend the pact or, absent agreement, signal intent to withdraw (triggering a 16-year “sunset” countdown)[2]. No concrete outcome by this date would push negotiations into an annual review cycle[2]. (In practice, insiders expect a painful extension with demands, not outright termination[2][17].)

Proposed Changes to Automotive Rules of Origin

Renegotiations center on modifying USMCA’s strict auto origin rules. The existing standards (USMCA Appendix 4-B) specify that passenger vehicles and light trucks must reach 75% regional value content (RVC) by 2023[18] and heavy trucks 70% by 2027[19]. A Labor Value Content (LVC) rule requires 40% (cars) or 45% (trucks) of value to come from facilities paying ≥US$16/hr[20][21]. Steel/aluminum inputs must be ≥70% North American by value[5]. The agreement also raised the content “de minimis” from 7% (NAFTA) to 10%[6].

RVC and LVC Thresholds

Current (USMCA): RVC for passenger vehicles 75% (100% by 2023)[18]; LVC 40% (cars) and 45% (trucks) by 2023[20][21]. The LVC rule (16$/hr wage floor) was phased in since 2020, reaching full effect in 2023[20][21]. Canada phased in its LVC later (30% since 2024)[22]. These requirements have already raised parts sourcing and wages in targeted plants via USMCA’s labor mechanism[23].

Proposals: U.S. officials reportedly seek tougher thresholds. Suggestions include raising RVC to 80–85% for cars and trucks (up from 75%) and/or narrowing “alternative staging” carve-outs[11]. Labor-content proposals (echoing President Trump’s 2018 demands) would push domestic/high-wage content to ≈50% of value[24]. In early USMCA talks (2018), the U.S. even proposed a 50% U.S. content requirement for autos[24]. While no finalized text changes exist yet, industry analyses anticipate that Washington will push for higher LVC (favoring U.S. & Canadian labor) and possibly tighter core-part rules. Mexico and Canada strongly oppose any measure that would make most autos ineligible: Canadian negotiators fear a 50% domestic-content rule “would devastate” their industry[24]. The exact wording remains under negotiation, but any increase means that more vehicles would fail to qualify for duty-free treatment, exposing their non-origin value to steep 25% tariffs[25].

Steel & Aluminum Sourcing; Other Provisions

Steel/Aluminum: Under USMCA, auto producers must certify ≥70% of steel and aluminum by value be sourced within North America[5]. Trump’s administration has already imposed 25–50% Section 232 tariffs on imported steel and aluminum from all countries (including NAFTA partners)[26]. In renegotiations, the U.S. may seek to broaden or enforce the steel/alum rule (for example, requiring U.S. origin specifically or raising the percentage).

De Minimis: The USMCA raised the tolerance for non-originating inputs (the “de minimis” allowance) from 7% to 10%[6]. No major proposals for this threshold have been reported; it may be left unchanged.

EV & Parts Classification: USMCA’s technical annexes define content rules for core auto parts. Emerging EV components have exposed gaps: e.g. e-axles and advanced batteries lack clear treatment, and battery cells are set at a 100% originating content threshold (impractical for many vehicles)[7]. The USITC noted that EV motors/inverters only require 50%[27], causing classification ambiguities. Renegotiators may clarify rules for batteries, electric motors, semiconductors, etc., to avoid conflicting HS classifications[27].

Impact on North American Supply Chains

North America’s auto supply chain is deeply integrated. Canada and Mexico provide a large share of the U.S. market: together they accounted for ~47% of U.S. light vehicle/parts imports in 2024[10], and about 74% of U.S. auto exports went to these neighbors[10]. Components routinely cross borders multiple times in a vehicle’s assembly. Figure above illustrates this integration.

Short-term: Tariff escalations (25% auto tariffs, 50% metal tariffs) have already disrupted supply chains. Automakers report diverting more production to the U.S. to avoid tariffs[8]. Some dealers say tariffs have added $5–10K per imported vehicle, on top of steel/alum costs that have increased vehicle prices ~$1.6–2K[28]. To illustrate, U.S. auto tariffs added an estimated $30B in costs in 2025[3]. The auto parts supplier lobby warned higher duties will raise consumer prices and cut sales[9]. Our analysis table (below) shows key pre- vs hypothetical post-renegotiation metrics.

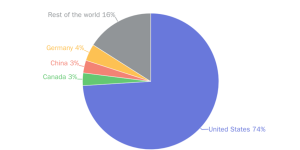

Figure: Mexican auto exports. Around 74% of Mexico’s passenger-vehicle exports (blue) go to the U.S. (gray), highlighting how any increase in U.S. tariffs or content rules would mainly affect Mexican production[29][1].

Figure: Mexican auto exports. Around 74% of Mexico’s passenger-vehicle exports (blue) go to the U.S. (gray), highlighting how any increase in U.S. tariffs or content rules would mainly affect Mexican production[29][1].

Supply-chain Adjustments: In response to tariffs, some manufacturers announced new U.S. plants: e.g. Toyota and Stellantis pledged multi-billion-dollar U.S. investments to shift production stateside[8]. Hyundai plans ~$26B in U.S. factories but says the uncertainty (including USMCA’s fate) delays decisions[30][31]. Conversely, automakers like BMW and Volkswagen have slowdowns in Mexico as they consider trade risk. A Canadian news report noted that since April 2025 Canada’s new 25% tariff on non-USMCA U.S. vehicles is encouraging imports from Mexico (where content passes)[32]. This reflects realignment of flows: Canadian auto imports from Mexico briefly exceeded those from the U.S. in summer 2025 once Canada’s tariffs took effect, before adjustments[32].

Parts and Materials: Suppliers in all countries are reassessing sourcing. The ROOs have encouraged some parts production to shift north: the USITC found that US parts output (and capital investment) rose under USMCA, at the expense of light-vehicle production[33]. If content requirements tighten further, suppliers may need to retool to source even more local inputs. Raw steelmakers see new demand: the Section 232 tariffs led about half of Mexican steelmakers (43 of 87) to cease U.S. exports by late 2025[34]. Canadian mills likewise pushed output to local markets. Overall, all three countries’ supply chains have seen supplier oversupply in some segments (e.g. certain parts) and idle capacity in others, pending regulatory clarity[8][9].

Effects on Production, Investment, Employment and Wages

Production Location: Heightened content rules and tariffs incentivize making vehicles closer to consumption. Many truck/SUV platforms are now slated for U.S. assembly (e.g. upcoming Ford, GM, Hyundai pickups). Toyota’s CFO admitted Section 232 made U.S. production more attractive[35]. However, passenger cars remain cheaper to build in Mexico; U.S. assembly wages are roughly $25–30/hr (much higher than Mexico’s $7–9/hr average). If LVC requirements rise, more production may shift to meet high-wage criteria, boosting U.S. plant utilization.

Investment: Automakers plan ~$50B in new North American investments (e.g. Hyundai $26B, Toyota $10B)[30], but many are contingent on stable trade rules[31]. As Greer notes, uncertainty has “deterred” capital spending[31]. Suppliers (parts makers) are similarly cautious: MEMA warns that an indecisive or protracted review will delay hiring and ordering of new tooling. Banks report an uptick in financing requests for North American projects as firms hedge future rule outcomes.

Employment and Wages: The auto sector is a major employer: roughly 1.3 million in Canada[36] and about 10–11 million nationwide in the U.S. including retail and service[14]. Mexican auto employment is estimated at ~2 million (≈11% of manufacturing labor)[37]. Stronger content rules would tend to shift some jobs north: USW notes that stagnating Mexican wages vs. U.S. wages incentivize offshoring, while the LVC rule’s $16/hr floor (above average Mexican pay) has already forced wage hikes at some Mexican plants via USMCA’s labor mechanism[12][23]. Indeed, USMCA’s rapid-response labor cases have secured wage increases and bonuses for thousands of Mexican auto workers[23]. However, experts warn that overly stringent wages (16$ threshold) could suppress competitiveness and push some Mexican production into informal labor[38]. In the U.S., automakers will likely face continued pressure (and union lobbying) to increase worker pay, but high import costs may dampen hiring.

Short-, Medium-, and Long-Term Impacts & Scenarios

- Short Term (1–2 years): Consumers face higher auto prices and limited choices. Dealers report average new-car prices up $5K–$10K due to tariffs[28]. Automakers adjust models and delay launches (especially EVs requiring extensive retooling to meet origin rules). Trade is volatile: in late 2025, U.S. auto imports from Mexico briefly surged (as observed in early Canadian data) before new tariffs were applied[32]. Some production is idled or flexed pending rule clarity.

- Medium Term (3–5 years): Investment is sensitive to trade policy. In a best-case renewal scenario, USMCA remains intact with minor tweaks (e.g. gradual phase-ins). Auto firms resume planned expansions, and North American content in vehicles stabilizes. If the U.S. gets tougher demands (the likely “painful extension”), the region may see a modest shift of production toward the U.S. and Canada, raising manufacturing costs (inflationary pressure) but boosting higher-wage jobs. Mexico’s growth could slow; firms may increase automation to meet content. Alternatively, if bilateral mini-deals replace trilateral (Trump’s preference), the supply chain could fracture: U.S.-Canada and U.S.-Mexico agreements might diverge on content, hurting pan-North American production.

- Long Term (6+ years): USMCA currently extends to 2036. If extended properly, long-run integration (especially for EV supply chains) remains strong. But if extended only reluctantly or by annual renewals, uncertainty lingers. In the worst case (withdrawal without a successor), the agreement would terminate (starting a 16-year “sunset” process). This would likely revert some trade frictions toward NAFTA-like tariffs and retaliation, severely disrupting the auto sector. According to CSIS scenario analysis, a renewal with moderate improvements would yield negligible GDP change but shift some welfare to North America; a painful extension would raise prices and slightly slow growth, while withdrawal could cause recessionary effects (through trade wars and supply-chain collapse)[33][39].

Quantitative Outlook: Key metrics include trade balances and tariff incidence. In 2024, NAFTA-region auto trade totaled ~$270 billion[10]. The U.S. ran a ~$108B deficit (imports $189B, exports $81B to CA+MX) in vehicles & parts[10]. If renegotiation raises content rules so that, say, 10% of current USMCA-origin vehicles fall out of compliance, up to ~$18B of U.S. imports could face a full 25% tariff (adding ~$4.5B in annual duties). Similarly, Canadian exports (~$46.5B) and Mexican exports ($104.8B) to the U.S. would incur tariffs on their ineligible portions. Table 1 below compares current and illustrative post-renegotiation values by country. (All figures are 2024 unless noted.)

Metric | United States | Canada | Mexico |

Vehicle exports to NA ($B) | $81 (2024)[10] | $46.5 (2024)[40] | $104.8 (2024)[37] |

Vehicle imports from NA ($B) | $189 (2024)[10] | ~$120 (incl. $18.9B from MX)[32] | $25.8 (2024)[41] |

U.S. trade balance (goods, $) | –$108B (deficit)[10] | ~$+25B (NAFTA vehicles) | +$79B (export surplus)[41] |

RVC requirement (cars) | 75% (2023)[18] | 75% (2023)[18] | 75% (2023)[18] |

LVC requirement (cars) | 40% (2023)[20] | 40% (2023) + 30% (2024)[22] | 30% (2023)[20] |

Steel/Alum NA source | 70% by value (since 2020)[5] | 70% (same) | 70% (same) |

De minimis threshold | 10% (raised)[6] | 10% (same) | 10% (same) |

Auto employment (millions) | ~10.95M (total jobs)[14] | 0.106M (direct jobs)[36] | ~2.0M (est., 11% of manuf.) (2024)[37] |

Avg. U.S. auto tariff on non-origin goods | 0% (USMCA) / 25% (new policy)[25] | 0% (USMCA) / 25% (on non-compliant imports) | 0% (USMCA) / 25% (on non-compliant imports) |

Impact of proposed RVC ↑5pp | Risk losing duty-free access on some exports | Higher non-origin content pays 25% tariff |

Note: “↑5pp” refers to raising RVC from 75→80%. Source data as cited.

Industry and Labor Perspectives

Automakers & Suppliers: Industry groups emphasize stability. The Alliance for Auto Innovation (OEMs+suppliers) warned in March 2025 that auto tariffs “will increase costs on consumers, lower vehicle sales… and reduce U.S. auto exports”[9]. At an industry summit, MEMA advised that a USMCA deal by July 1 is unlikely, urging members to prepare for a “drawn out, politically charged process”[42]. In Reuters interviews, top executives expressed concern: Ford’s CEO Farley said the integrated North American system is “critical” but needs “revisions,” lamenting “whiplash” of tariff flips[43][44]. Toyota said the 25% tariffs make investment decisions “hard to justify” without trade certainty[8]. Hyundai, which plans a new U.S. truck plant, estimated that an immediate USMCA extension would unlock ~$20B in U.S. investment[30]. Volkswagen insisted any USMCA 2.0 “must recognize integrated supply chains,” and Nissan observed that higher U.S. labor costs make entry-level models more expensive under tariffs[45][35].

Unions & Labor: Labor groups uniformly back tightening content/labor rules. United Auto Workers representatives have publicly welcomed tariffs and called for “renegotiation of trade deals, including USMCA” to protect jobs[46]. The U.S. Steelworkers (USW) testified to USTR that widened trade deficits and stagnant Mexican wages demand reopening USMCA[12]. USW noted Mexico’s failure to improve labor standards under USMCA and blasted “loopholes” allowing Chinese content via Mexico[47]. Similarly, the Alliance for American Manufacturing (AAM) submitted detailed comments advocating for “closing loopholes” in origin rules and blocking non-market (China) content[13][48]. AAM warned that Chinese firms are “rushing to route content through Mexico,” threatening an “extinction-level event” for U.S. autos[13][48]. Labor groups urge raising the LVC and enforcing the Rapid-Response Labor Mechanism, noting the thousands of Mexican auto workers who gained wages via USMCA enforcement[23]. AFL-CIO has similarly argued for tighter rules to stop “backdoor” Chinese imports.

Suppliers: Parts makers share OEM concerns. The Motor & Equipment Manufacturers Association (MEMA) and others emphasize that supply chains cannot be reconstituted overnight[9]. They plead for predictability: AHT auto suppliers warned that abrupt rule changes would force costly requalification of parts and even plant closures. Some battery and semiconductor suppliers, key to EVs, fear new content tests could slow EV rollouts.

Policy and Compliance Considerations

Manufacturers must prepare for swift policy shifts. Any change to origin rules means re-assessing product compliance: new content tracking, renegotiating contracts, and re-certifying NA origin for each model. For example, raising RVC to 80% could render several recent models non-originating; companies would then pay 25% tariffs or source more parts from high-cost locations. Compliance teams will need to analyze which models drop out and develop strategies (e.g. redesign or pay duty). Regulators (CBP) may issue new guidelines on labor-content calculation if LVC is adjusted.

Policy risks are high: Trump’s administration has repeatedly overridden NAFTA/USMCA panels (e.g. auto ROO dispute) in favor of unilateral tariffs[49]. If formal renegotiation stalls, the U.S. could continue use Section 232/IEEPA tariffs to pressure Canada/Mexico (as seen in 2025[50]). In turn, Canada and Mexico have signaled frustration: LeBlanc pressed for immediate tariff relief on steel/alum, dairy, etc., even outside USMCA talks[51]. The risk of side deals looms: Trump openly suggested splitting USMCA into separate U.S.-Mexico and U.S.-Canada agreements[52]. Manufacturers must thus track multiple forums (WTO disputes, bilateral negotiators, domestic rulemakings) simultaneously.

Regulatory complexity will rise if a new pact sets divergent rules with Canada vs. Mexico (Greer indicated separate “protocols”[53]). For example, if Canada agrees to one set of automaker demands and Mexico another, North American automakers may have to build different vehicle specs or maintain dual supply chains. The possible introduction of higher CUSMA (Canada-US-Mex) content or labor quotas could also complicate trade planning. Compliance groups should advise leadership on contingency tariffs: e.g. how much new duty each model could incur under various RVC/LVC scenarios.

Strategic Recommendations

- For Automakers & Suppliers: Intensify scenario planning. Map current content margins for each vehicle and part: identify those at risk if RVC or LVC rise. Invest in automation and workforce upskilling to raise productivity (thus meeting higher LVC without huge wage bills). Consider diversifying sourcing: e.g. explore U.S. parts suppliers or near-shoring in Canada to raise regional content. Engage proactively with negotiators: share data on cost impacts. Preserve flexibility: design future platforms for multiple assembly options (U.S. or Mexico).

- For Policymakers: Balance objectives. While stronger content rules can boost domestic jobs, overly aggressive changes risk inflating prices and driving investment elsewhere. The U.S. should coordinate with Mexico/Canada on China-related measures to avoid a game of one-upmanship. Support workers through transition: invest in training for high-tech automotive jobs (EVs, batteries) to align labor conditions. Consider gradual phase-ins or waivers (as originally in USMCA) rather than abrupt cuts, to give industry time. Maintain trust by respecting dispute resolution (alternatives to unilateral tariffs) to keep partners engaged.

- Shared Priorities: All parties should aim to preserve integrated supply chains. A breakup of USMCA would inflict heavy cost on consumers and industry alike. Instead, focus on targeted fixes: e.g. tighten enforcement of existing labor provisions (RRM)[23], curb abuses (e.g. Chinese circumvention) through FDI screening rather than wholesale rule changes, and align on common threats like EV content standards. Transparency will help: publish negotiating texts and allow industry input on technical issues (EV classifications, input sourcing) to avoid unforeseen barriers.

Data Gaps and Assumptions: Our analysis uses available 2024 trade figures and reported proposals (e.g. Bloomberg, Reuters interviews) to sketch likely scenarios. Actual outcomes will depend on final political compromises. Precise quantitative impacts (like exact tariff cost changes) are model-based and would require firm-level origin data. We assume Trump’s tariff regime persists through the review. Any policy reversal (e.g. lowering Section 232 tariffs) would alter cost analyses significantly.

Sources: Official USMCA texts and government reports (USITC, trade.gov), recent news releases (Reuters, USITC), industry publications, and policy analyses (CSIS, Alliance for Auto Innovation, Alliance for American Manufacturing) were used throughout[18][2][8][3][26][33][9]. Key data on trade flows and content rules are cited in tables and figures above. These sources reflect the state of negotiations as of early 2026. Any deviations in actual July 2026 outcomes should be adjusted accordingly.

[1] [15] [51] [52] Canada calls discussions with US on USMCA ‘constructive’ | Reuters

[2] [16] [42] [53] USTR Greer says US-Mexico-Canada pact talks may run past July 1 deadline | Reuters

[3] Auto tariff to cost US consumers more than $30 bln in first year, report shows | Reuters

[4] [28] Auto Tariffs Have Added $30 Billion in Costs, Driving Up Vehicle Prices: Tariff Tracker | Digital Dealer

https://digitaldealer.com/news/us-tariff-tracker-impact-automaker-response/164521/

[5] [6] [18] [19] [20] [21] USMCA Auto Report

https://www.trade.gov/usmca-auto-report

[7] [27] [33] USITC Releases Second Report on the Economic Impact and Operation of the USMCA Automotive Rules of Origin | United States International Trade Commission

https://www.usitc.gov/press_room/news_release/2025/er0701_67239.htm

[8] [30] [31] [35] [45] Automakers plan billions in US investments but seek clear trade rules | Reuters

[9] Statement on Auto Industry Tariffs | Alliance for Automotive Innovation

https://www.autosinnovate.org/posts/press-release/auto-tariffs-3-28-25

[10] Top U.S. Trade Goods with Canada & Mexico | Greenbrier

[11] [34] USMCA Automotive Rules of Origin: Economic Impact and Operation, 2025 Report

https://www.usitc.gov/publications/332/pub5642.pdf

[12] [47] [48] Steelworkers Tell USTR: Renegotiate the USMCA – Alliance for American Manufacturing

https://www.americanmanufacturing.org/blog/steelworkers-tell-ustr-renegotiate-the-usmca/

[13] AAM Sees Plenty of Room for Improvement in the USMCA – Alliance for American Manufacturing

https://www.americanmanufacturing.org/blog/aam-sees-plenty-of-room-for-improvement-in-the-usmca/

[14] Driving US Economy and Innovation | Alliance For Automotive Innovation

https://www.autosinnovate.org/initiatives/the-industry

[17] [23] [26] [38] [39] [49] [50] USMCA Review 2026

https://www.csis.org/analysis/usmca-review-2026

http://www.cvma.ca/industry/facts/

[24] Challenges and opportunities for the North American auto industry …

[25] A Guide to Trump’s Section 232 Tariffs, in Maps | Council on Foreign Relations

https://www.cfr.org/articles/guide-trumps-section-232-tariffs-nine-maps

[29] [37] [41] Mexico – Automotive Industry

https://www.trade.gov/country-commercial-guides/mexico-automotive-industry

[32] Canada imported more vehicles from Mexico than the US in June

https://mexiconewsdaily.com/business/canada-imported-more-vehicles-mexico-us-june/

[43] [44] Ford CEO says trade deal with Mexico and Canada is ‘critical’ for industry | Reuters

[46] UAW Statement on Tariffs and Renegotiating U.S. Trade Agreements – UAW | United Automobile, Aerospace and Agricultural Implement Workers of America

https://uaw.org/uaw-statement-on-tariffs-and-renegotiating-u-s-trade-agreements/